Alternative Data and Its Role in Amplifying Financial Development in Africa

Africa’s financial landscape is a complex and dynamic mix of traditional banking services and cutting-edge digital innovations. This diversity reflects the continent’s vast array of cultures, languages, and economic conditions. From the bustling cities to the rural heartlands, access to financial services varies greatly. In urban areas, traditional banking is more accessible, while many rural regions lack basic banking facilities. This disparity has left a substantial portion of the population unbanked, without access to fundamental financial services.

The mobile revolution has been instrumental in bridging this gap. This innovation has enabled millions to access financial services via mobile phones, bypassing traditional banking infrastructure. Africa’s leadership in mobile money accounts is a testament to its rapid adaptation to digital solutions, making it a global frontrunner in this space.

In this blog post, we will delve deeper into the transformative capabilities of AI in empowering both customers and businesses in the African banking sector, with a particular focus on how AI-driven alternative credit scoring models can help overcome the challenge of limited access to banking.

Economic Landscape and Demographic Dynamics

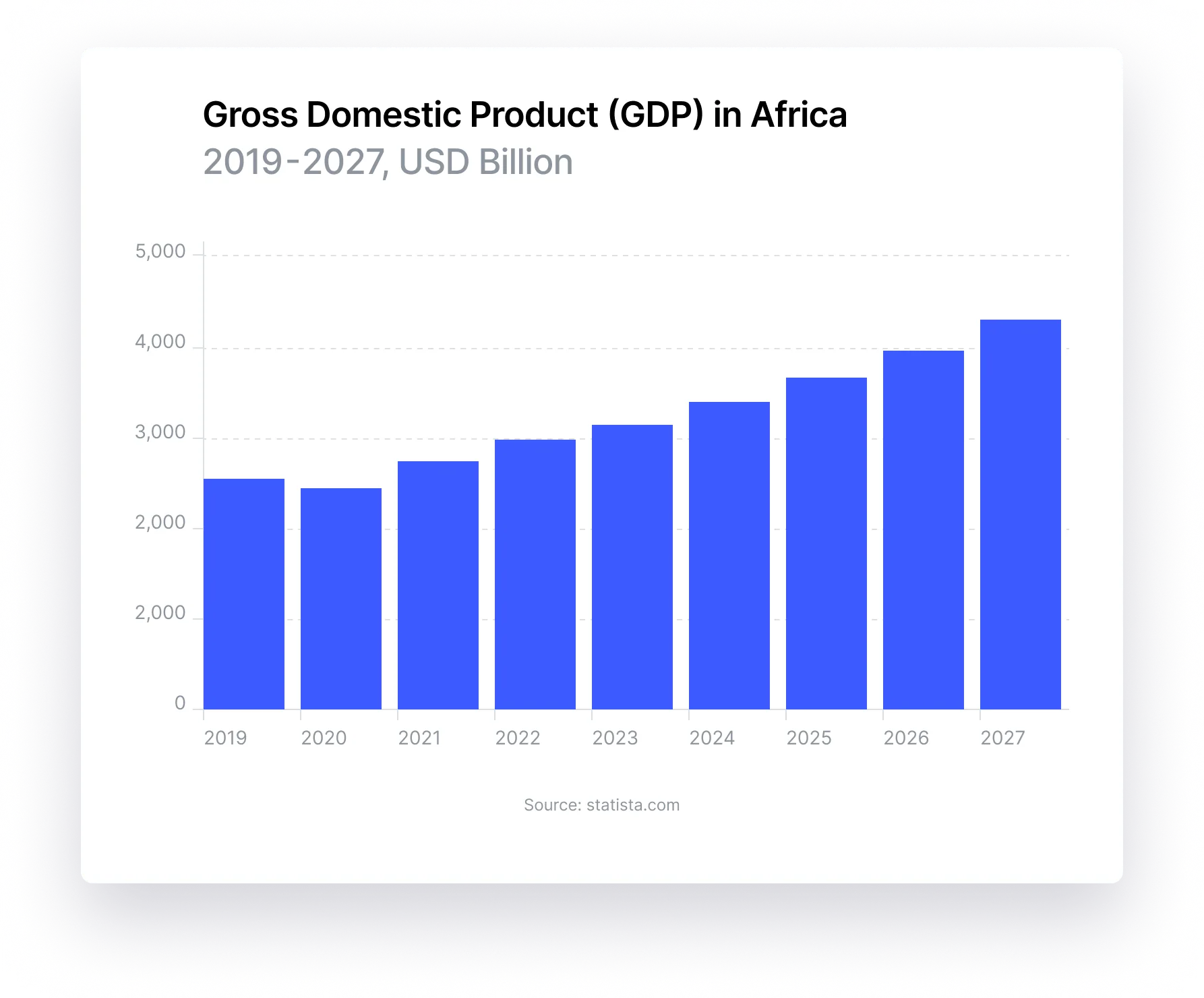

The African economy, particularly in Sub-Saharan Africa, has shown remarkable resilience during the pandemic. The region experienced a GDP decline of 1.9% in 2020, one of the most severe recessions in recent decades. However, a rebound was expected in 2021, with a projected real GDP growth of 3.4%, indicating a reopening of the region’s potential for financial innovation.

The African economy was recovering from the COVID-19 pandemic in 2022 when it encountered a range of internal and external shocks, including the impact of a global crisis. Although Africa’s direct trade and financial connections with various regions were minimal, these challenges exacerbated the continent’s economic difficulties. They led to increased commodity prices and escalated food and fuel inflation, contributing to a rise in civil strife amid heightened political instability. Key African economies like South Africa and Nigeria, already grappling with low growth, faced increased debt burdens, with some nations’ dollar debts reaching distressed levels. The public sector debt-to-GDP ratio in African countries was over 60% in 2022. These developments suggest a shift in the economic landscape, with potential implications for various projects and investments, including those related to initiatives like the Belt and Road Initiative.

The interplay of global economic slowdown and post-pandemic recovery challenges, including those stemming from recent international tensions, have imposed significant strains on Africa’s sustainable development journey. The continent has experienced rising inflation, notably in the cost of food and energy, which disproportionately impacts the economically vulnerable by elevating the prices of vital goods. This situation exemplifies the broader economic pressures faced by African nations, many of which depend on imports for essential commodities such as oil, maize, and wheat. The compounded effects of global economic uncertainties and health crises have underscored the critical need for resilient and adaptive economic strategies in Africa. These dynamics highlight the interconnectedness of global events and their capacity to exacerbate existing socio-economic challenges, urging a comprehensive analysis that transcends specific geopolitical conflicts to encompass the wider global economic landscape’s impact on Africa’s development and sustainability goals.

Key Challenges in the Financial Sector

Despite advancements in mobile banking, the African financial sector faces several significant challenges:

1. Limited Access to Banking

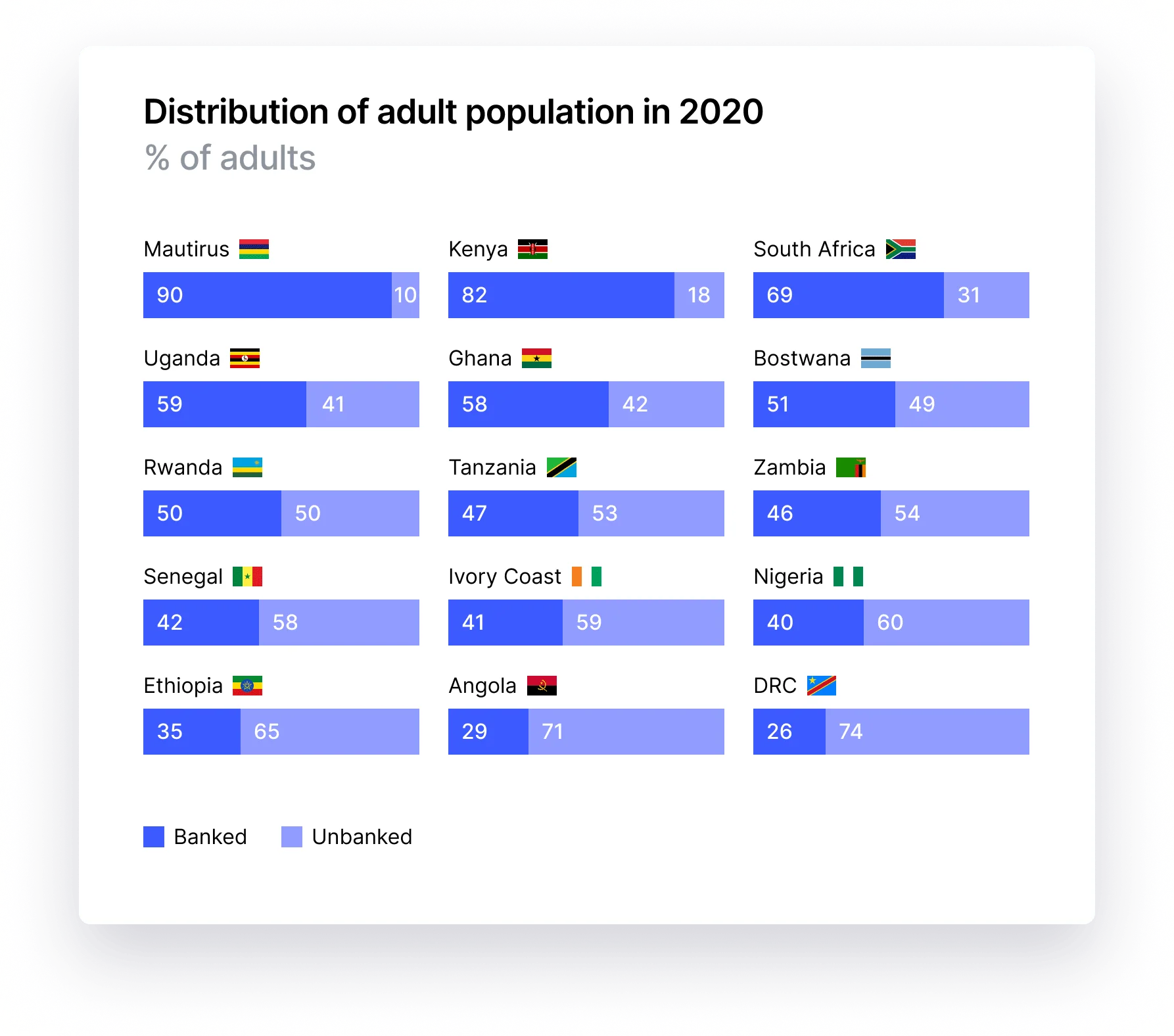

Although 48% of Africa’s population now uses banking services, a large portion, particularly in rural areas, still lacks adequate access to banking facilities. This gap in access hinders engagement in the formal financial system and reflects the significant divide between urban and rural financial services availability.

2. High Costs of Financial Services

The cost of financial services across Africa remains a barrier, especially for low-income individuals. These costs can deter people from maintaining bank accounts or accessing credit, further widening the financial inclusion gap.

Banking markets show considerable variability across the continent. In more mature markets like South Africa, Mauritius, and Kenya, banking penetration is relatively high. However, a large part of the Sub-Saharan population remains unbanked, with countries like Nigeria, Ethiopia, Tanzania, and the Democratic Republic of Congo exhibiting low banking penetration.

3. Underdeveloped Financial Infrastructure

Many African regions still lack essential financial infrastructure. This includes a shortage of ATMs, banking branches, and digital payment platforms, which impedes the delivery of financial services to a broader population.

The disparity in urbanization rates also plays a critical role in financial inclusion. With an average urbanization rate of only 41%, many African countries have not yet fully urbanized, impacting the distribution and accessibility of financial services.

4. Financial Literacy Gap

There is a notable deficiency in financial literacy across the continent. This gap affects the population’s ability to make informed financial decisions and effectively use available financial services.

These challenges and potential solutions underscore the urgent need for innovative approaches to enhance financial inclusion and literacy, and to develop more accessible and affordable financial services across the continent.

To address them, banks and other industry players could reconsider their channel strategies, integrating digital and human experiences, and enhancing their B2C offerings by digitizing end-to-end processes for operational efficiency. This could result in significant cost reductions across various functions and improve customer-facing sales and care.

Artificial Intelligence (AI) is indeed playing a pivotal role in addressing the challenge of access to banking services in Africa. AI can streamline complex processes, offer personalized customer experiences, and provide data-driven insights for better decision-making. In the upcoming sections, we will delve deeper into the transformative capabilities of AI in empowering both customers and businesses in the African banking sector.

Unlocking Financial Inclusion Through AI and Alternative Data

As we’ve seen, traditional credit scoring models have served their purpose but leave a significant portion of the population underserved, both in the United States and globally. The challenges posed by changing financial dynamics, the gig economy, digital banking, and more have necessitated a reevaluation of how we assess creditworthiness. In Africa, where limited access to banking is a prominent issue, the adoption of alternative credit scoring methods driven by Artificial Intelligence (AI) holds great promise.

The Power of Alternative Data

Alternative credit scoring models delve beyond the traditional parameters of credit history, offering a more inclusive approach. They consider non-traditional data sources such as social media profiles, online behavior, mobile usage, online shopping habits, etc. These unconventional data points provide a more comprehensive view of an individual’s financial behavior, allowing lenders to assess credit risk and predict borrowing behavior more accurately.

Learn More About Alternative Credit Scoring

AI-Driven Machine Learning Algorithms

AI and machine learning algorithms play a pivotal role in harnessing the potential of alternative data. By analyzing vast datasets encompassing past financial behavior, loans, debts, and repayment patterns, AI identifies subtle trends and patterns within a borrower’s history that might go unnoticed in traditional models. These insights enable lenders to enhance the quality of their credit scores, making lending decisions more informed and nuanced.

Collaboration with Third-Party Providers

Utility companies, rental agencies, and other service providers hold a treasure trove of data regarding an individual’s payment history. Collaborative efforts with these entities allow for a deeper analysis of how borrowers manage their financial responsibilities over time. This information goes beyond mere credit history and delves into the day-to-day financial interactions of individuals, offering a more holistic view of their creditworthiness.

Customized Models for Specific Populations

One of the key advantages of alternative credit scoring system is the ability to create customized models tailored to specific population groups. This approach recognizes that individuals may have unique financial profiles due to factors such as self-employment, age, relocation, or past financial issues. By tailoring credit scoring models to these distinct segments, lenders can make more accurate lending decisions and extend credit to a wider range of borrowers.

Leveraging Alternative Credit Scoring for Financial Inclusion

In the context of Africa’s limited access to banking services, alternative credit scoring models powered by AI offer a lifeline to millions. By tapping into non-traditional data sources, machine learning algorithms, and collaborations with service providers, these models can bridge the financial inclusion gap.

Moreover, understanding credit risk more accurately opens doors to tailored loan rates and terms, increasing the number of loans disbursed and identifying new customer markets. This not only benefits borrowers but also contributes to the growth of the financial sector in Africa.

Wrapping Up

AI-driven alternative credit scoring models have the potential to revolutionize the way financial institutions assess creditworthiness, particularly in regions like Africa where access to traditional banking services is limited. Embracing these innovative approaches can empower individuals and businesses by providing them with better access to credit, ultimately fostering economic growth and financial stability across the continent.

If you are excited about the potential of AI-driven alternative credit scoring models to unlock financial inclusion in Africa and want to explore how GiniMachine can assist your organization in implementing these transformative solutions, we encourage you to get in touch with our team.