Unleashing Financial Empowerment with GiniMachine: A Fresh Lifeline for Lenders to Serve Unbanked Borrowers

In a world where financial stability is fundamental to individual prosperity, a significant portion of the global population remains ‘unbanked’ or ‘underbanked’, disconnected from the traditional banking ecosystem. These groups face steep obstacles in accessing credit facilities, often forcing them to resort to costly and less secure alternatives. However, with the advent of artificial intelligence and machine learning, we are on the brink of a transformative shift that can bridge these financial divides.

GiniMachine is leading the charge in this arena. By leveraging non-traditional data sources and sophisticated machine learning algorithms, it opens up new avenues of financial empowerment for the lenders to serve unbanked and underbanked in some countries also called invisible borrowers. This technology not only presents a fresh lifeline for these borrowers, but it also enables lenders to safely tap into this largely ignored market segment, thus fostering greater financial inclusion globally.

In this article, we explore how lenders can leverage GiniMachine to capture a new market niche and expand financial access to the ‘unbanked’. We delve into the intricacies of this often overlooked group and how, with the help of GiniMachine’s paradigm-shifting credit scoring, lenders can not only reach but also sustainably serve this sector. Let’s dive in.

Clarifying the ‘Banked,’ ‘Underbanked,’ and ‘Unbanked’

The complexities of financial access and stability necessitate clear definitions and understanding of banking terminologies. The terms ‘banked,’ ‘underbanked,’ and ‘unbanked’ are essential in these discussions, particularly in highlighting the disparities in financial inclusion.

1. Banked

‘Banked’ individuals have access to a comprehensive array of financial services via their banking accounts, which typically include savings and checking accounts, credit cards, loans, and more. Owing to their established financial status, ‘banked’ individuals enjoy a wealth of benefits including security, convenience, and the potential to earn income through interest. Moreover, they have an easy pathway to credit and loans, resulting from a saturated market full of lenders and banks vying to offer them services. The competition in this sector is intense, which often leads to more favorable terms for such borrowers.

2. Underbanked

The ‘underbanked’ are those who, despite having a bank account, find themselves frequently resorting to alternative and often costly financial services. The Federal Deposit Insurance Corporation (FDIC) categorizes an individual as ‘underbanked’ if they have a bank account but also rely on services like payday loans, check cashing, and money transfers due to limited access to comprehensive banking services. Challenges like geographical constraints, inadequate access to digital banking platforms, or the perceived high costs and complexities of banking can force them into this category.

This category of borrowers presents a unique challenge to lenders. With traditional credit assessment tools falling short, the inherent risk of default often overshadows the potential benefits of serving this market. As such, the underbanked space has remained largely uncompetitive, with many lenders hesitant to engage due to the high risk involved.

3. Unbanked

The ‘unbanked’ are individuals who lack any form of relationship with traditional banking institutions. These individuals, as defined by the FDIC, do not hold a checking or savings account and primarily transact in cash, storing their assets in physical, offline forms. Reasons for being ‘unbanked’ can range from voluntary choices driven by distrust of banks or worries about bank fees to unavoidable barriers such as lack of a permanent address or the inability to provide required identification.

Much like the ‘underbanked’, the ‘unbanked’ present a significant challenge for lenders due to the inherent difficulties in assessing creditworthiness with traditional tools. This leads to a high risk of default and subsequently, sparse competition in this segment. However, GiniMachine offers a solution to this problem. Employing alternative data and sophisticated models, it allows lenders to venture into this untapped market, effectively mitigating risks and expanding financial inclusion. Consequently, with GiniMachine, lenders can begin catering to these underserved borrower categories, significantly reducing default risk through robust predictive modeling.

By leveraging alternative data and advanced models, lenders can tap into this market, mitigating risks, and increasing financial inclusion. GiniMachine’s potential in this space is exemplified by telecom enterprise, where alternative data was effectively used to serve an ‘unbanked’ population. With GiniMachine, lenders have the opportunity to transform this challenging niche into a profitable venture.

The unbanked and underbanked populations often find themselves trapped in a cycle of costly alternative financial services, potentially predatory lending, and limited opportunities to build credit or savings. Financial institutions, policymakers, and technology innovators are continuously exploring solutions to bridge these gaps and promote broader financial inclusion.

GiniMachine, with its AI-powered approach to credit scoring, are examples of how technology can help overcome traditional barriers and pave the way for a more financially inclusive future while ensuring that lenders get the high ROI.

There is currently no up-to-date data on this matter, but we have made an effort to gather the information that is available in order to provide an illustration of the number of individuals who fall into the category of being “unbanked” in various regions across the globe.

- Latin America and the Caribbean: According to the World Bank’s Findex database, approximately 26% of adults in Latin America and the Caribbean did not have a bank account as of 2021. According to a client based in Brazil, the proportion of individuals without access to banking services or with limited access, can potentially reach as high as 50% in this country. It’s clear that the unbanked population is a significant part of the target audience for lenders in this region.

- Sub-Saharan Africa: Statista reports that about 45% of Sub-Saharan Africa’s adult population was unbanked in 2021. However, the region is experiencing a rapid increase in mobile money accounts, indicating a shift toward non-traditional banking solutions.

- Middle East and North Africa: As of 2017, an estimated 67% of adults in the Middle East and North Africa region remained unbanked according to the World Bank.

- South Asia: The World Bank stated that in 2021, about 32% of adults in South Asia didn’t have a bank account.

- East Asia and the Pacific: As per the World Bank’s data, around 29% of the adult population in this region did not have a bank account.

- The US: In 2021, around 5.9 million households in the United States, accounting for an estimated 4.5%, were classified as “unbanked,” indicating that none of the individuals within those households possessed a checking or savings account at a bank or credit union.

Learn More About AI Decision-Making Software

GiniMachine: A New Dawn for Unbanked Borrowers

GiniMachine applies AI and machine learning algorithms to evaluate creditworthiness, even when there’s a lack of traditional credit history. It uses alternative data sources, like mobile phone usage, utility bill payments, or even social media behavior, to create a comprehensive and accurate credit profile. Traditional credit scoring methods, such as the FICO model, focus on credit history, financial history, and other similar factors to ascertain the likelihood of default on payments by a borrower. However, these traditional models, which have remained largely unchanged since their inception in 1989, often exclude a significant number of individuals — over 28 million Americans are credit invisible, and an additional 21 million are deemed unscorable. This signals a significant shortcoming in traditional credit scoring, which is where alternative credit scoring and tools like GiniMachine come in.

GiniMachine makes those borrowers ‘visible.’ By bypassing the traditional need for a credit history and instead focusing on alternative data, these borrowers can start to build a credit profile. The AI’s ability to analyze and predict based on unconventional data gives these individuals a foot in the door of the banking world they have been historically denied.

GiniMachine’s algorithms provide the unique ability to tailor credit scoring models for specific groups. These may include the self-employed, younger or older individuals, or those who have relocated or faced financial issues in the past. Such bespoke credit scoring models yield more precise results, fostering greater confidence in lending to these often underrepresented demographics.

Furthermore, GiniMachine’s system has been designed to incorporate diverse data sources, which the client can independently secure. While GiniMachine does not provide the data, it is equipped to process information from third-party collaborations that clients may establish with utility companies, rental agencies, and other service providers. This flexibility enables lenders to gain a holistic view of a borrower’s payment history, providing valuable insights into creditworthiness beyond traditional credit history. This more complete picture of a borrower’s financial responsibility can lead to more accurate and inclusive lending decisions.

See How It Applies in Real Life: A Story From Our Client MobiCom

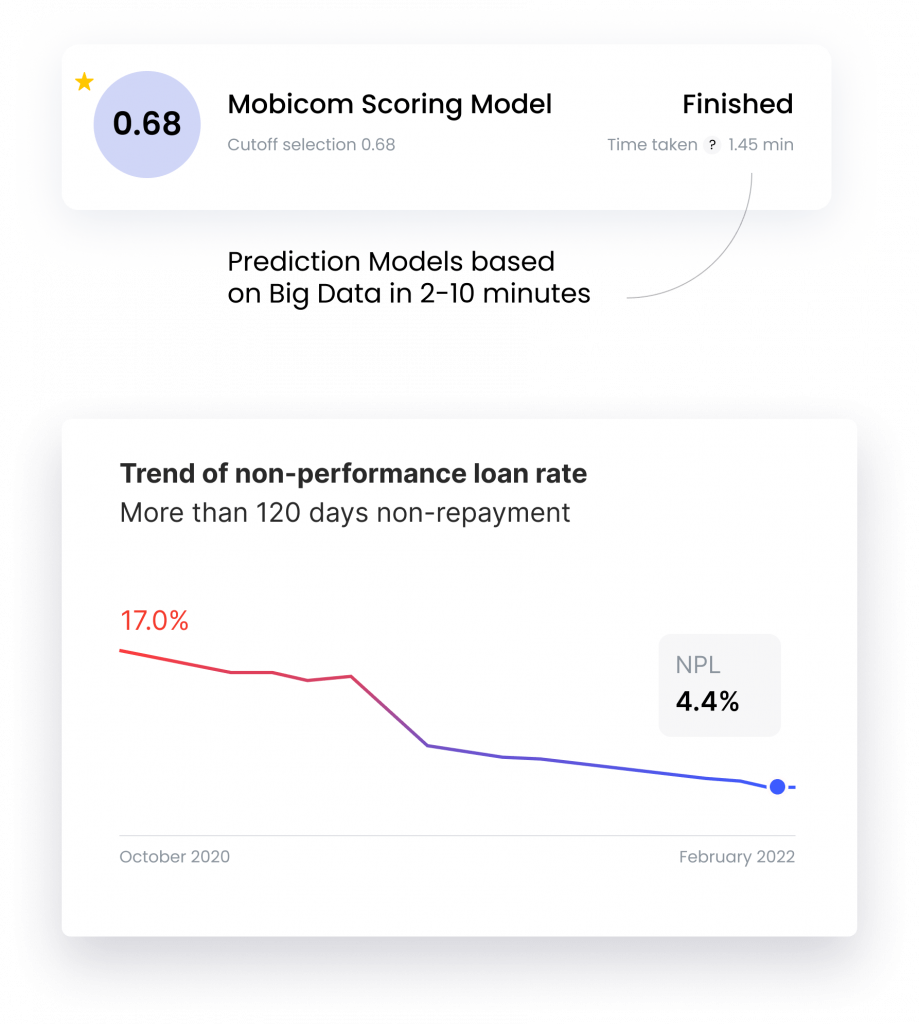

MobiCom Corporation, a Mongolian-Japanese telecom venture, faced challenges with their existing credit scoring system, including high labor intensity, inefficiency, and a high Non-Performing Loans (NPL) rate of 18.9%. They needed a solution that could efficiently manage big data, process imperfect data, and generate precise predictive models.

GiniMachine provided the perfect solution. Implementing a blend of heuristic methods and custom decision tree ensemble method, we automated their data preprocessing, freeing up their team for more complex tasks. GiniMachine swiftly created and validated a scoring model, which helped reduce MobiCom’s NPL rate fourfold to 4.4% in just 17 months, improving loan approval speed and risk-profit balance.

Despite initial challenges in deploying the credit scoring system on-premises, GiniMachine delivered a high-performing credit scoring software capable of handling big and unstructured data and creating reliable prediction models. The result: lower NPL rates, higher loan acceptance, and valuable data insights for MobiCom.

You can read more about the MobiCom case.

Wrapping Up

The ‘unbanked’ and ‘underbanked’ represent a significant untapped market for financial service providers. Harnessing GiniMachine’s advanced AI and machine learning capabilities, lenders can safely and effectively extend their services to these often overlooked consumers and small businesses. Despite the lack of traditional credit history, lenders can accrue a larger volume of loans, build greater trust with customers, and cultivate a reputation as a reliable lender, thereby fostering financial inclusivity.

As the MobiCom case study illustrates, GiniMachine not only reduces the NPL rates but also provides reliable prediction models and valuable insights into lenders’ data.

Take the first step towards a more financially inclusive future for your organization. GiniMachine is offering a free trial, giving you the opportunity to experience first-hand the transformative power of our AI-driven credit scoring system.

Interested in learning more? Get in touch with the GiniMachine team today to get access to a free trial, giving you the opportunity to experience first-hand the transformative power of our AI-driven credit scoring system.