One of the recent exciting updates at GiniMachine that we are eager to introduce is the cross-validation feature. Below we break down how it is applied and in what way it can be valuable for your finance business.

When and What for Cross-Validation Is Used

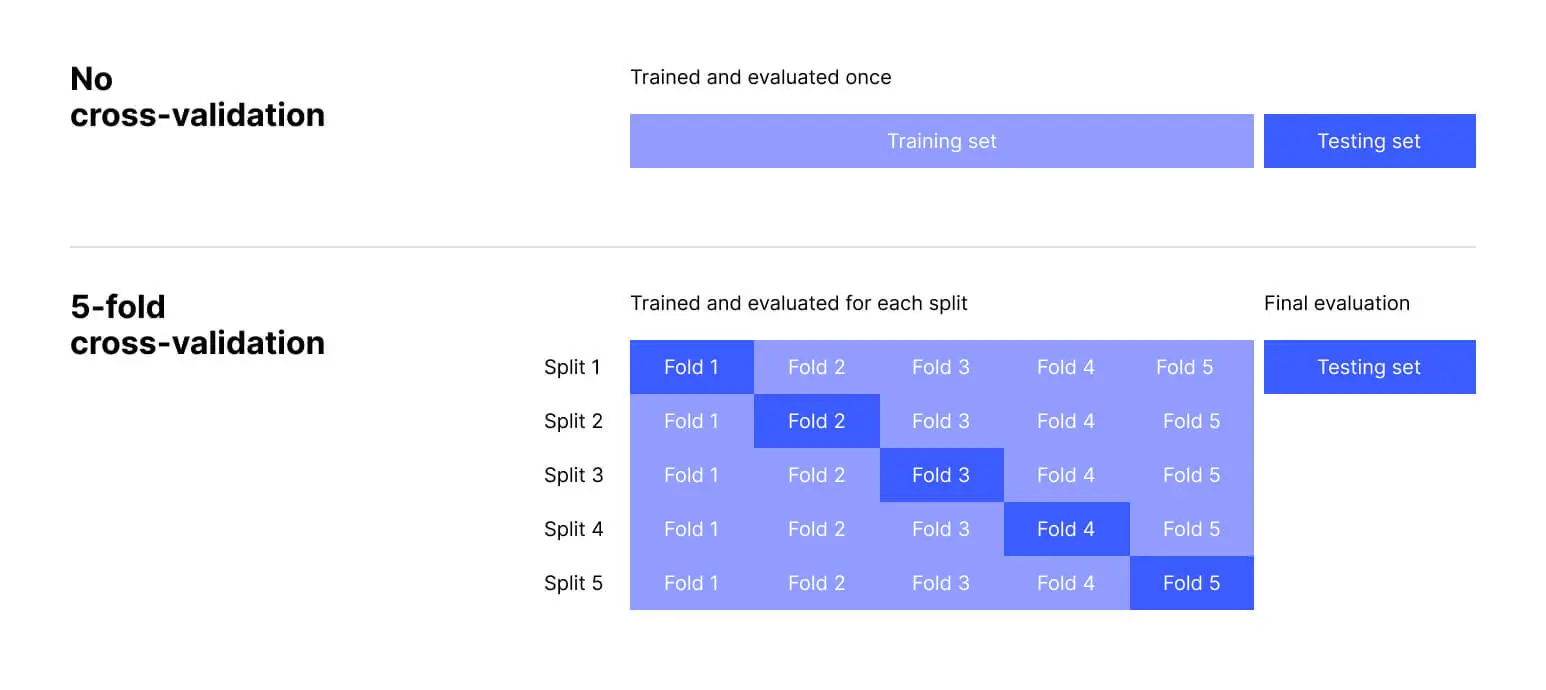

On a general note, cross-validation is a model validation technique that tests how a predictive model performs on unseen data. Instead of building a model on one training set and evaluating it once, cross-validation repeatedly splits the historical dataset into training and validation parts and averages the results.

This approach is especially important in credit scoring, where historical loan data may be limited. By using multiple splits, cross-validation maximizes the use of all available data for both training and testing while still ensuring that each evaluation is done on data the model has never seen. The result is a more robust assessment of model performance that reflects how the model might generalize to new loans, rather than an overly optimistic estimate from reusing the same training sample.

By offering stratified 5-fold cross-validation, GiniMachine equips financial institutions with a practical tool to satisfy both BIS and ECB model validation requirements, particularly in terms of robust validation of the accuracy and consistency of PD estimates, out-of-sample testing, and overfitting control.

In a typical 5-fold cross-validation (as shown above), the dataset is divided into five equal ‘folds.’ The model is trained on four of the five folds and tested on the remaining fold, and this cycle is repeated five times, so that each fold serves as the test set once.

Every loan in the dataset ends up in a test fold exactly once, ensuring the model is evaluated on fresh data during each iteration. Finally, the models from all five runs are aggregated to obtain a more accurate and stable final scoring model.

How GiniMachine Implements Stratified Splitting

With a range of approaches in cross-validation, GiniMachine landed in stratified splitting. That means, folds are created to preserve the same class proportions (for example, the ratio of ‘good’ vs ‘bad’ loans) in each subset. In practice, this means each fold is a microcosm of the overall dataset.

For instance, if roughly 20% of loans in the historical data resulted in default (bad loans), then about 20% of each fold will also be bad loans. Maintaining this balance in every fold ensures the validation results are fair and representative of the full portfolio, even when classes are imbalanced. Stratification prevents scenarios where one validation split might, by chance, contain too few or too many bad loans, which could skew the performance results. By mirroring the overall distribution of outcomes, each fold provides a realistic test, leading to more reliable accuracy and risk metrics.

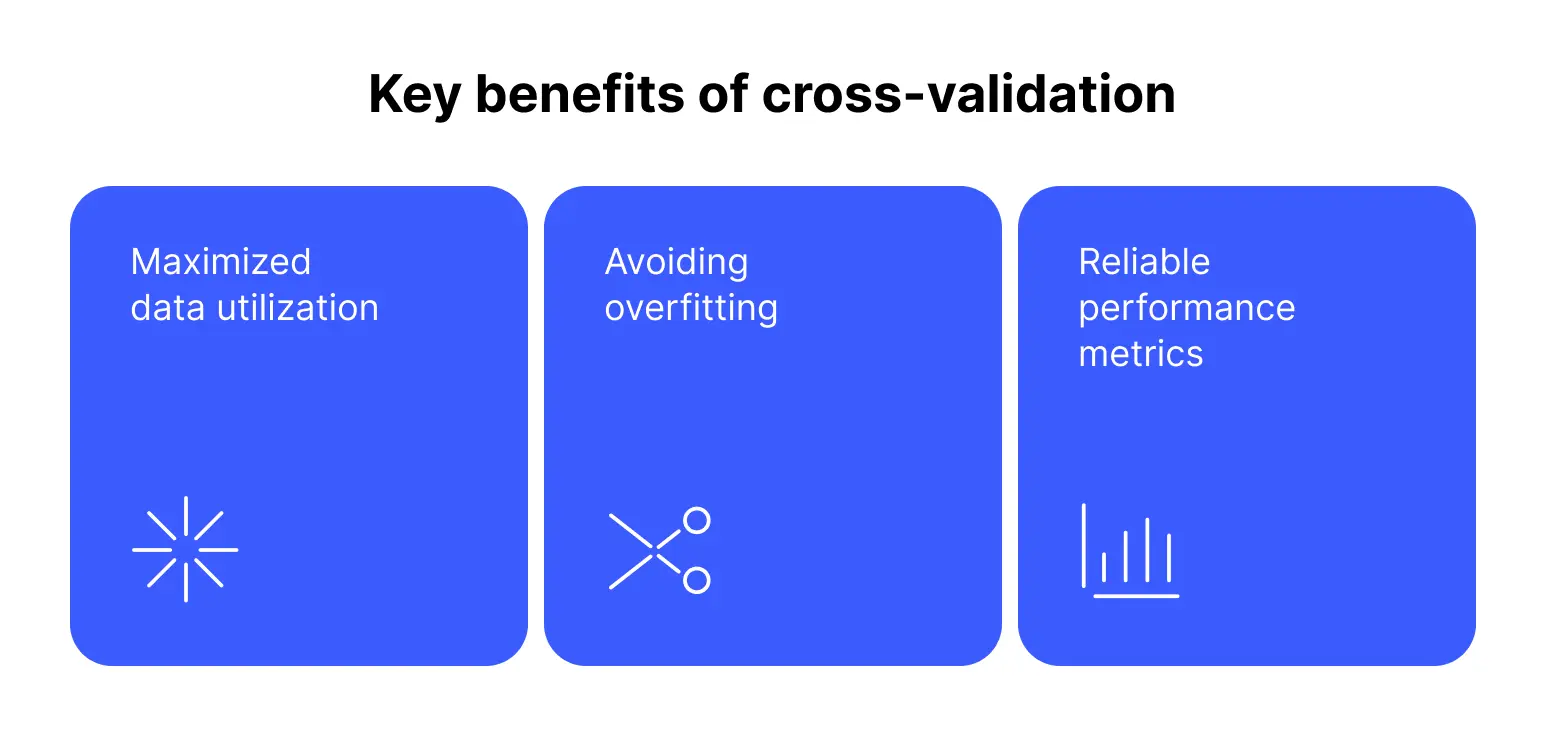

Key Benefits Of Cross-Validation

In credit scoring, the true test of a model is how well it performs on data it has never seen before. That’s where cross-validation comes in.

- Maximized data utilization: cross-validation makes the most of limited historical data. Every record is used for training in some folds and for validation in another, so no data is wasted. This approach allows the model to be tested on all observations over the course of the procedure (just at different times), providing more information than a single split would.

- Avoiding overfitting: by ensuring the model is evaluated on unseen data in each fold, cross-validation helps guard against overfitting (the model “memorizing” the training data). The model must prove it can predict new loan outcomes in every round, which means we can be confident it’s learning genuine patterns rather than just the quirks of one training set.

- Reliable performance metrics: Because cross-validation tests the model multiple times on different slices of data, the resulting model is more robust. Averaging results across folds gives a realistic estimate of model accuracy, reducing the chance that an unusually easy or hard single test split misleads us.

Similarly, multiple probability calibrations (which show how closely predicted probabilities of default match actual observed default rates) are computed using truly out-of-sample predictions, so they’re not biased by the training data. In short, cross-validation provides a dependable gauge of how the model will perform and how well it’s calibrated on new loans, rather than on the data it was trained on.

Conclusion

Cross-validation is thus a crucial part of Model Evaluation and Calibration functionality in GiniMachine. It ensures that a credit scoring model is rigorously vetted from all angles before deployment.

By using stratified 5-fold cross-validation, GiniMachine delivers performance and calibration insights that can be trusted to reflect real-world behavior, giving credit analysts and risk managers confidence in their model’s stability and predictive power.

For a more comprehensive approach, GiniMachine can be integrated into debt collection management software, enhancing it with AI tech and giving FinTech businesses an extra advantage over their competitors.